.svg)

.webp)

Afin d'atteindre les objectifs fixés par le Pacte Vert (Green Deal) européen, l'Union européenne produit de plus en plus de législations liées à l'ESG. Il devient donc difficile de naviguer dans le paysage juridique ESG qui est aujourd'hui presque aussi complexe que la législation financière. Ceci est logique puisque l'objectif principal du Pacte Vert est d'appréhender ces deux aspects ensemble afin de mettre en place une « nouvelle stratégie de croissance vis(ant) à transformer l’UE en une société juste et prospère, dotée d’une économie moderne, efficace dans l’utilisation des ressources et compétitive » (Communication de la Commission européenne - Le Pacte Vert pour l'Europe). Cette feuille de route s'inscrit notamment dans le cadre des Accords de Paris de 2015 ratifiés par l'UE et visant à limiter le réchauffement climatique en dessous de 2C° par rapport à l'ère pré-industrielle.

La Corporate Sustainability Reporting Directive (CSRD) est l'un des principaux instruments permettant de mettre en place cette stratégie, car elle fixe des normes élevées pour le reporting en matière de développement durable, afin de pouvoir comparer les entreprises sur leurs performances ESG, en plus de leurs performances financières. Mais comment la CSRD s'articule-t-elle avec les autres législations ESG telles que la CSDDD, la loi européenne sur le climat ou la SFDR ?

Cet article explique comment la CSRD est liée aux législations suivantes :

- Loi européenne sur le climat

- SFDR

- Pilier 3

- Règlement sur les indices de référence

- Taxonomie durable

- CSDDD

La loi européenne sur le climat : le pilier du Pacte Vert

La loi européenne sur le climat est un règlement adopté en 2019 dont le but principal est d’établir un “objectif contraignant de neutralité climatique dans l’Union d’ici à 2050” (Article 1, §2 de la loi européenne sur le climat). Il s’agit donc d’un texte particulièrement important pour l’Union européenne dans sa stratégie de développement durable.

Pour atteindre cet objectif, plusieurs leviers ont été identifiés, tels que:

- La contribution de tous les secteurs économiques

- La transition vers un système énergétique sûr, durable, abordable et sécurisé

- La transformation numérique, l'innovation technologique et la recherche et le développement

- Les puits de carbone, en particulier dans les secteurs de l'agriculture, de la sylviculture et de l'utilisation des terres

L'Union européenne et les États membres encouragent (ou obligent) les acteurs économiques à contribuer à la fois au travers de leur cadre réglementaire et par leurs investissements durables sur le plan environnemental. Le CSRD fait partie de ce cadre réglementaire puisqu'elle exige des entreprises qu'elles publient des informations sur leur stratégie climatique.

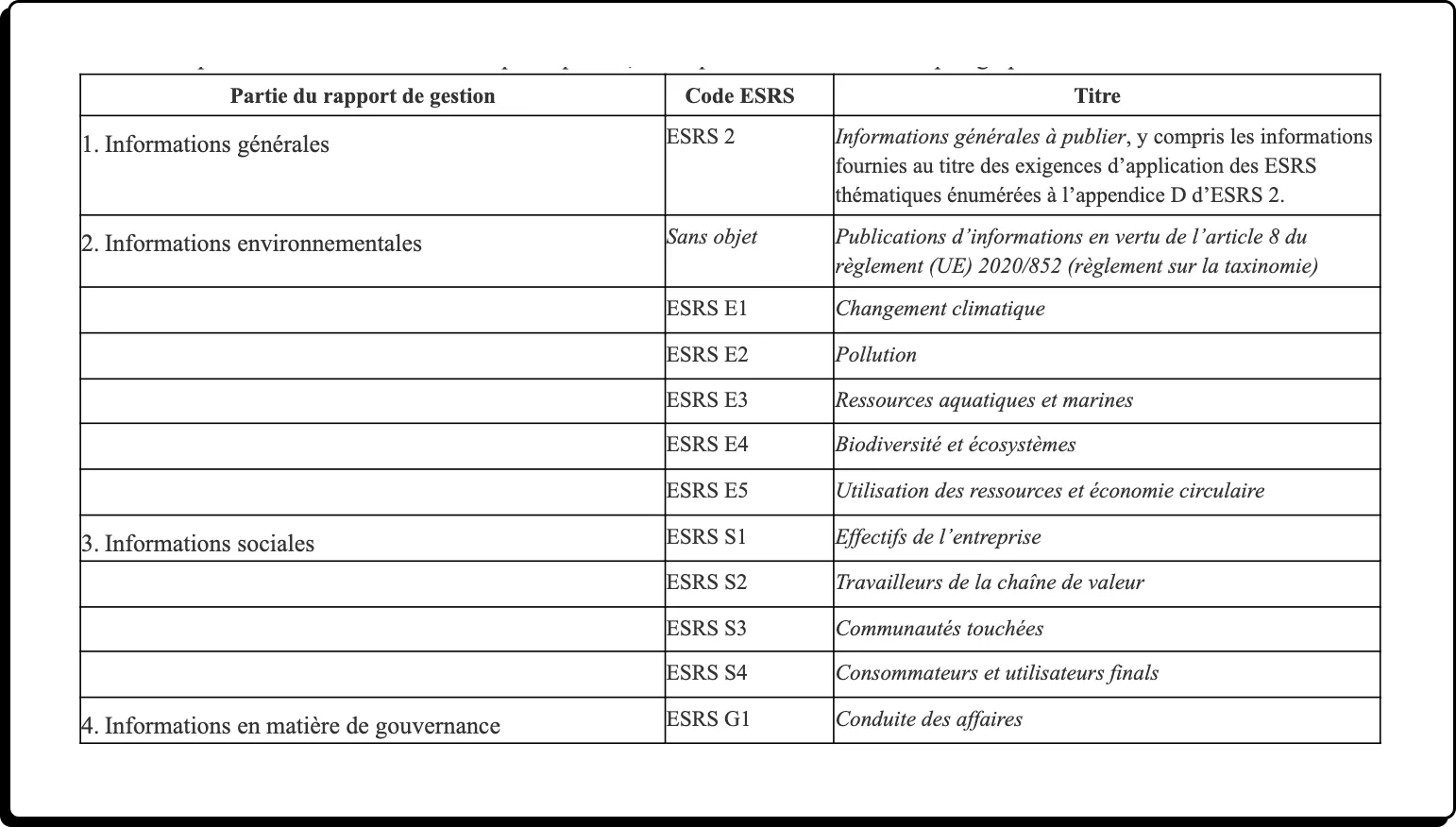

Les ESRS sont directement liés à la loi européenne sur le climat étant donné que l’ESRS 2 dispose que les entreprises doivent inclure dans leur rapport “un tableau de tous les points de données qui découlent d’autres actes législatifs de l’UE (incluant la loi européenne sur le climat) en précisant où ils figurent dans la déclaration relative à la durabilité et en incluant ceux qu’elle considère, après évaluation, comme n’étant pas importants, en indiquant, dans ce cas, « pas importants » dans le tableau” (ESRS 2, IRO-2, §56).

Deux points de données de la loi européennes sur le climat sont mappés dans l'appendice B de l’ESRS 2:

- ESRS E1-1 (§14) Plan de transition pour atteindre la neutralité climatique d’ici à 2050

- ESRS E1-7 (§ 56) Absorptions de GES et crédits carbone

Son lien avec les législations pour une finance plus durable

La SFDR, le règlement Pilier 3 et le règlement sur les indices de référence sont trois législations qui concernent toutes le secteur financier et ont différents objectifs. En complément de la loi européenne sur le climat, il s’agit des trois autres législations qui sont mappées avec les ESRS et qui font partie des exigences sur le tableau des points de données qui découlent d’autres actes législatifs de l’UE (exigence de publication IRO-2).

1 - La SFDR

La Sustainable Finance Disclosure Regulation (SFDR) “établit des règles harmonisées pour les acteurs des marchés financiers et les conseillers financiers relatives à la transparence en ce qui concerne l’intégration des risques en matière de durabilité et la prise en compte des incidences négatives en matière de durabilité dans leurs processus ainsi que la fourniture d’informations en matière de durabilité en ce qui concerne les produits financiers” (Article 1).

Ce règlement établit trois types de fonds sur lesquels les acteurs financiers doivent divulguer des informations spécifiques dans leurs informations pré-contractuelles :

- Fonds “Article 6” qui ne promeuvent pas d’objectifs durables particuliers

- Fonds “Article 8” qui font la promotion de caractéristiques environnementales ou sociales

- Fonds “Article 9” qui sont les investissements considérés comme durables

Selon la SFDR, les acteurs des marchés doivent publier des informations sur la manière dont leurs produits financiers prennent en compte les principales incidences négatives en termes de durabilité. Pour ce faire, la Commission a publié en 2022 un règlement délégué qui définit certains indicateurs que les acteurs des marchés doivent considérer lors de l'estimation des principales incidences négatives en termes de durabilité liées aux entreprises dans lesquelles leurs produits visent à investir.

Ces indicateurs incluent des métriques environnementales et sociales souvent obligatoires au titre de la CSRD (cf. mapping de l’ESRS 2, Appendice B). Dès lors, le tableau des points de données liés à la SFDR que les entreprises divulgueront au titre de l’ESRS 2 IRO-2, comme mentionné précédemment, sera particulièrement utile pour les acteurs de marchés afin de collecter les informations nécessaires au calcul des incidences négatives de leurs investissements.

2 - Le règlement Pilier 3

Le règlement Pilier 3 établit des exigences prudentielles pour les établissements, les compagnies financières holding et les compagnies financières holding mixtes. Les exigences prudentielles visent à rendre le secteur financier plus stable, tout en veillant à ce qu'il soit en mesure de soutenir les ménages, les entreprises et les autres utilisateurs finaux de services financiers.

Ces exigences prudentielles sont très larges. Elles incluent la divulgation des risques environnementaux, sociaux et de gouvernance des établissements qui ont émis des actions admises à la négociation sur des marchés réglementés d’un Etat membre. Étant donné que ces établissements sont souvent concernés par la CSRD, les divulgations connexes sont mappées dans l’Appendice B de l’ESRS 2. La plupart de ces exigences sont liées à l’ESRS E1 sur le changement climatique.

Pour les points de données connexes, les établissements qui doivent répondre aux exigences de divulgation de leurs risques environnementaux, sociaux et de gouvernance conformément au règlement Pilier 3, ont la possibilité, dans leur rapport de durabilité de la CSRD, d’incorporer ces informations par référence aux divulgations Pilier 3 s’ils s’assurent que les périmètres de consolidation sont les mêmes pour les deux rapports.

3 - Le règlement sur les indices de référence

Le règlement sur les indices de référence “instaure un cadre commun visant à garantir l'exactitude et l'intégrité des indices utilisés comme indices de référence dans le cadre d'instruments et de contrats financiers, ou pour mesurer la performance de fonds d'investissement dans l'Union” (Article 1).

Ce règlement est lié à la CSRD étant donné que les administrateurs d’indices de référence financiers doivent expliquer comment les facteurs ESG sont reflétés dans chacun de leurs indices ou familles d’indices. Par exemple, les administrateurs d’indices de référence “transition climatique” de l’Union et “accords de Paris” sont encouragés à augmenter la part des émetteurs des titres constitutifs qui fixent et publient des objectifs de réduction des émissions de gaz à effet de serre dans leurs indices.

Le lien entre la loi européenne sur le climat et la taxonomie durable

La taxonomie durable (aussi appelée taxonomie verte ou taxonomie européenne) établit un système de classification doté de définitions claires qui déterminent ce qu’est une activité environnementalement durable dans le but d’aider les investisseurs et les entreprises à prendre des décisions éclairées d’investissement.

A travers des critères techniques s’appliquant à des secteurs d’activité spécifiques, il est possible de déterminer si une activité contribue à un ou plusieurs des objectifs environnementaux suivants :

- Atténuation du changement climatique

- Adaptation au changement climatique

- Utilisation durable et protection des ressources aquatiques et marines

- Transition vers une économie circulaire

- Prévention et réduction de la pollution

- Protection et restauration de la biodiversité et des écosystèmes

Pour répondre aux exigences du règlement sur la taxonomie durable, les entreprises doivent divulguer certains KPIs :

- La part de leur chiffre d’affaires provenant de produits ou de services associés à des activités économiques pouvant être considérées comme durables sur le plan environnemental

- La part de leur CaPex liée à des actifs ou à des processus associés à des activités économiques pouvant être considérées comme durables sur le plan environnemental

- La part de leur OpEx liée à des actifs ou à des processus associés à des activités économiques pouvant être considérées comme durables sur le plan environnemental

Au titre de l’ESRS 1, ces obligations de divulgations de la taxonomie doivent être incluses dans le rapport de durabilité de la CSRD dans une section séparée :

Il y a plusieurs autres références additionnelles à la taxonomie durable dans les ESRS environnementaux. Par exemple, l’exigence de publication E1-1 (Plan de transition pour l’atténuation du changement climatique) exige que les entreprises qui ont des activités économiques couvertes par la taxonomie divulguent “une explication de tout objectif ou plan (CapEX, plans CapEx, OpEX) que l’entreprise s’est fixé pour aligner ses activités économiques (revenus, CapEx, OpEX) sur les critères établis dans le règlement” sur la taxonomie.

Par ailleurs, il y a un lien entre la taxonomie et la SFDR. En effet, lorsqu’un produit financier investit dans une activité économique qui contribue à des objectifs environnementaux, des informations sur les critères de la taxonomie doivent être incluses dans les informations pré-contractuelles.

Ses liens avec la CSDDD et le rapport de durabilité de la CSRD

Ses liens avec la CSDDD et le rapport de durabilité de la CSRD

Enfin, la Corporate Sustainability Due Diligence Directive est la dernière législation ESG importante adoptée par l’Union européenne. Elle concerne les très grandes entreprises seulement donc le périmètre est plus restreint que celui de la CSRD.

Alors que la CSRD établit une obligation de divulguer de l’information, la CSDDD établit une obligation passer à l’action par :

- la mise en oeuvre d’une due diligence en termes de risques relatifs aux droits de l’Homme et à l’environnement

- l’adoption et la mise en oeuvre d’un plan de transition climatique pour s’assurer que l’entreprise met les moyens nécessaires pour aligner son business model et sa stratégie avec la limitation du réchauffement climatique à 1,5 °C et avec l’objectif de neutralité climatique fixé par la loi européenne sur le climat

Les sanctions sont basées sur le chiffre d'affaires mondial des entreprises. Le pourcentage sera défini par les États membres et pourra aller jusqu'à un maximum de 5 % du chiffre d'affaires. Par ailleurs, si les obligations de vigilance ne sont pas respectées et qu'un préjudice est causé à une personne physique ou morale, les entreprises pourront être tenues responsables civilement et devront alors verser des indemnités.

Beaucoup de personnes pensent que la CSDDD établit de nouvelles exigences de divulgation. Néanmoins, “pour éviter de dupliquer les obligations de déclaration”, la CSDDD dispose que la directive “ne devrait pas instaurer de nouvelles obligations en la matière en sus de celles prévues prévues par la directive 2013/34/UE (CSRD)”. Donc, une entreprise qui est soumise à la CSRD en plus de la CSDDD devra divulguer les informations sur la façon dont elle répond aux exigences de la CSDDD dans son rapport de durabilité au titre de la CSRD.

Étant donné que les ESRS ont été adoptés avant la CSDDD, ils ne mentionnent pas cette législation. Néanmoins, il y a de nombreuses exigences de publication qui sont pertinentes pour divulguer la façon dont les entreprises mettent en œuvre la CSDDD. Concernant le devoir de vigilance, la section 4 de l’ESRS 1 y est dédiée et établit un mapping entre les éléments essentiels de due diligence et les exigences de publication de l’ESRS 2 et, dans certains cas, celles des ESRS thématiques. Concernant les objectifs climatiques, le plan de transition climatique requis par la CSDDD sera divulgué sous l’exigence de publication E1-1 (Plan de transition pour l’atténuation du changement climatique).

Pour conclure, la loi européenne sur le climat vise à accélérer la transition verte de l'Union européenne tout en lui permettant de modifier en profondeur son économie et notamment de devenir un des leaders mondiaux dans le domaine de l'industrie verte. En s'appuyant à la fois sur une transparence accrue, une mobilisation de fonds privés et d'un plan de relance européen, elle vise à accompagner les entreprises dans cette transition tout en créant de nouvelles opportunités économiques et favorisant le développement d'emplois verts.