What is CSRD?

The CSRD, or Corporate Sustainability Reporting Directive, is a European directive concerning the publication of extra-financial data by companies. It replaces the Non Financial Reporting Directive ( NFRD), which until now has provided a relatively vague framework for the publication of CSR data by companies.

It aims to strengthen companies' transparency obligations and assess their impact on ESG criteria, as well as their level of commitment to environmental and social issues.

The CSRD goes a long way towards specifying the non-financial reporting expected of companies, while at the same time broadening the number of organizations concerned by this reporting. By leaving less room for interpretation regarding the data expected and their level of precision, the CSRD aims to make publicly disclosed information more exhaustive and reliable, particularly for investors:

- By standardizing non-financial reporting through the introduction of Europe-wide reporting standards, the ESRS, defined by EFRAG. Until now, companies were free to choose which standard they wished to follow. This will make it easier to compare the reporting of different companies, thanks to a common language, and will also enable automated processing of reports.

- By making it compulsory for reports to be audited by the Statutory Auditor - or by an Independent Third-Party Body, at the discretion of each EU member state - who will be responsible for verifying the reliability of published information and reporting formats.

- By extending the scope of companies concerned, which will be five times greater than that of the NFRD. Reporting will thus cover more than 50,000 companies.

Launched as part of the Green Deal for Europe, this new directive aims to redirect investment flows towards projects in line with the sustainable development objectives defined by the European Union. They are therefore in line with new European standards such as the SFDR (Sustainable Finance Disclosure Regulation) on sustainable finance and the European taxonomy that has set up a classification of activities.

This reporting work will be mandatory for companies covered by the scope, and the penalties incurred will be set by each member country by the end of 2023.

Who is affected by the CSRD?

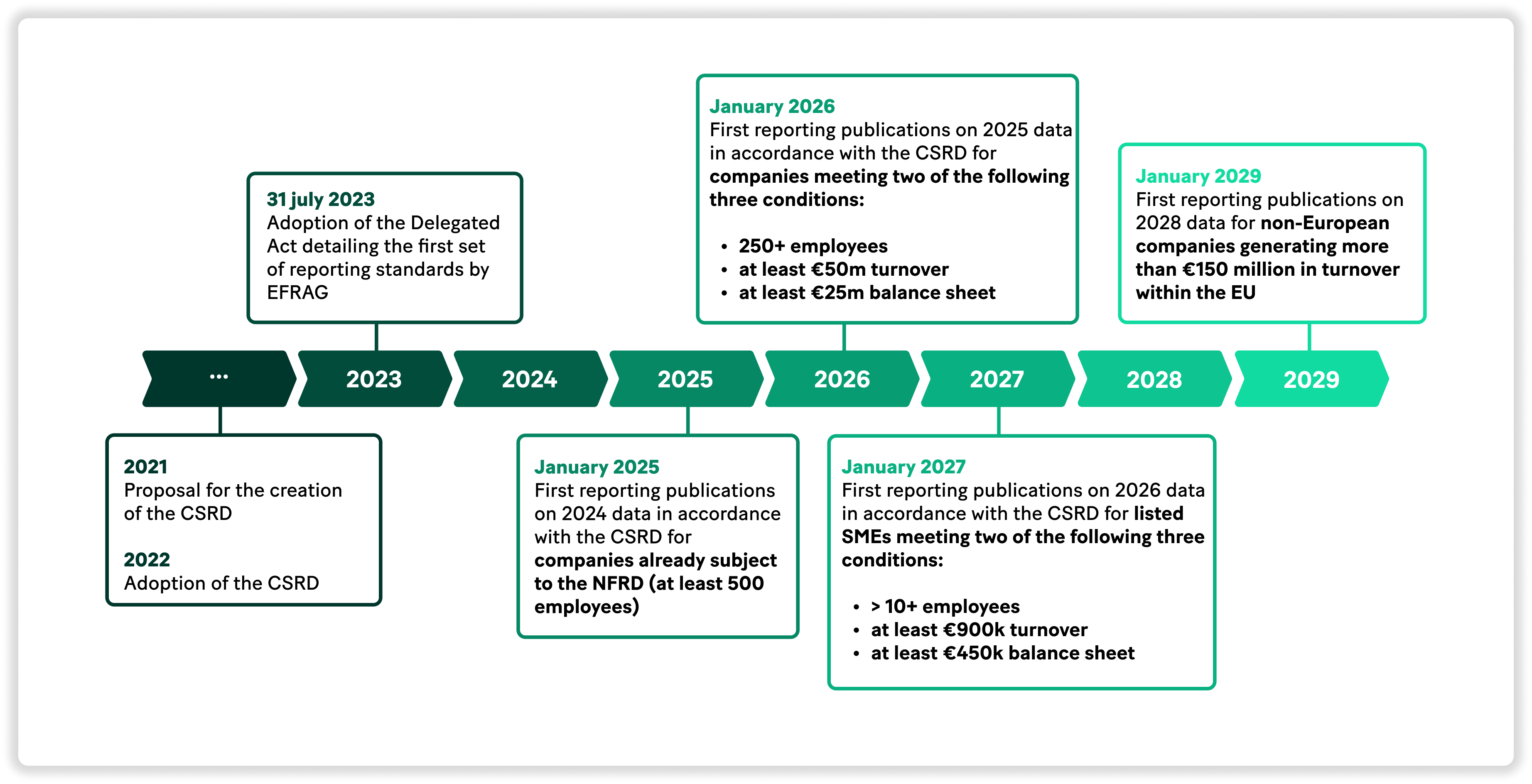

The CSRD will be rolled out progressively, starting in January 2024 with companies currently subject to the NFRD. Eventually, this ESG reporting obligation will be extended to more than 50,000 European and non-European companies active within the EU.

European companies

The European entities concerned by this new reporting obligation are those that meet at least two of the following three criteria:

- Employ 250 or more employees.

- Generate sales of 50 million euros or more.

- Have a balance sheet of €25 million or more.

This also applies to SMEs listed on European markets that meet at least two of the following three criteria:

- 10 or more employees,

- Generate sales of 900,000 euros or more.

- Have a balance sheet of 450,000 euros or more.

As part of their commitment to transparency, unlisted SMEs will also be able to publish their extra-financial data within the same framework.

Non-European companies

Non-European companies generating net sales of over €150 million in the EU will also be required to publish data on the sustainability of their activities.

What information on climate change should be included in the reporting?

EFRAG, the European Financial Reporting Advisory Group, recently published a first set of reporting standards for CSRD. The set of data is divided into 12 separate documents, the ESRS, each of which addresses a specific reporting topic around CSR, Corporate Social Responsibility:

Each document describes the information and content expected in the extra-financial report on a specific social and environmental topic. This includes both quantitative and qualitative data, enabling us to take stock of the current situation and measure the company's present and future commitment to CSR issues. This is analyzed in particular through the efforts made in terms of governance and the integration of these issues into the company's development strategy.

Below is a summary of the "Climate Change" document and the content that would a priori be requested by the CSRD on the specific subject of climate change (climate change mitigation and adaptation):

Carbon footprint and transition action plan.

In the section of the CSRD report related to climate change, the company will have to present:

- Its impact on the climate, i.e. its carbon footprint. The standard to be followed will be that of the GHG protocol and GRI 305. Emissions must be accounted for across the entire value chain, covering scope 1, scope 2 and scope 3.

- Its capacity to adapt to climate change as currently projected (+1.5°C), but also to climate change predicted by less optimistic scenarios. It should specify the company's risks and opportunities (financial and physical) linked to climate change.

Objectives, trajectories and commitments.

Each company will have to set out a trajectory for reducing its GHG emissions, and will also have to explain how it will achieve its targets. Companies will have to present :

- A target compatible with a +1.5°C trajectory, in line with the Paris agreements, which will be defined by an emissions reduction target, also specifying whether it is based on science, as well as actions taken (past, present and future) and their impact (past, present and future) on the company's emissions.

- A trajectory to 2030, or even 2050 if possible, with a revision of the target and a redefinition of the reference year every five years from 2030 onwards.

Each company will also have to justify the consistency of its transition plan with its business and financial strategy.

The means allocated to the implementation of the transition plan.

The report should also include a full summary of the transition plan, and present the financial resources invested in this transition plan, in particular communicating the significant volumes of CapEx and OpEx mobilized.

Companies will also be required to report annually on their progress in implementing their transition plan.

Company policies.

In order to explain how the company is able to implement its climate transition plan, the company's environment-related policies will have to be set out along five axes:

- Climate change mitigation,

- Adaptation to climate change,

- Energy efficiency,

- Deployment of renewable energy,

- Miscellaneous for the remaining topics.

The company's energy mix.

Companies will have to disclose their absolute energy consumption, as well as their energy mix. A clear separation of energy consumption by energy source should be detailed for companies in sectors with a high climate impact, by communicating:

-> On the one hand, on the consumption of non-renewable energy sources,

- Coal,

- Petroleum fuels,

- Gas,

- Other fuels,

- Nuclear products,

- Electricity, heating network, steam network, cooling network of non-renewable origin,

-> On the other hand, on the consumption of energy from renewable sources,

- Biogas,

- Electricity, heating network, steam network, cooling network of renewable origin,

- Internal power generation.

Funding for GHG sequestration and climate change mitigation projects.

Companies will also have to report on the amount of GHGs removed from the atmosphere and sequestered on a long-term basis. They should be distinguished according to the type of project:

- GHG sequestration within the company's value chain,

- GHG sequestration through projects financed outside the company's value chain.

The aim of this directive is not only to measure a company's ability to contribute to the net zero objective, but also to provide a framework for public communications on this subject, thus avoiding the temptation of Greenwashing.

The internal price of carbon.

Where applicable, companies that have introduced an internal carbon pricing system should explain the system in place and its scope: activities and entities covered, quantity of GHGs by categorization (scope 1, 2 or 3), calculation methodology.

The important notion of Dual Materiality.

A very important notion required in the CSRD is the approach to all the points mentioned above through that of dual-materiality. Each company will have to explain in its report not only how it is impacted by climate change, but also how this impacts its activities and its transition plan (physical and financial impacts across the company's entire value chain). In this way, the company will have to present a rigorous analysis of the risks and opportunities associated with climate change, and justify its capacity to adapt to climate change. This section of the report will include an analysis of the positive and negative financial impacts of climate change:

- Potential financial impacts related to physical hazards (e.g., risks of water stress, fire outbreaks),

- The potential financial impact of the company's inherent transition risks (e.g. cost trends, new legislation),

- The ability to seize any new opportunities arising from climate change.

CSRD Calendar: Key dates.

The deployment of this new obligation will be progressive until 2026 depending on the size of the company.

To help companies with this first publication exercise, EFRAG plans to publish standards and drafting guidelines in two stages.

- July 31, 2023: publication of the delegated act containing the first 12 cross-functional ESRSs and the CSRD reporting standards

- 2024: publication of directives specific to SMEs, more proportionate to their size

- 2026: adoption of sector standards (initially scheduled for June 20, 2024)

- 2026: adoption of standards dedicated to non-European companies, which will have to report in 2029 on 2028 data

What penalties apply?

Each EU member state will be responsible for defining the sanctions applicable in the event of non-compliance with CSRD obligations when transposing the directive into national legislation.

On December 7, 2023, France became the first country to transcribe the CSRD directive into national law, withOrdinance No. 2023-1142. This retranscription includes a list of penalties for companies that fail to meet their obligations under the CSRD.

In the event of non-compliance with their obligations, the sanctions introduced in France are as follows:

- Injunction under fine: any person may apply for an injunction under fine to compel the production, communication or transmission of documents or information relating to sustainability.

- The exclusion from public procurement of companies that fail to meet their obligation to publish sustainability information. This sanction will apply from January 1, 2026.

- Criminal liability of the director and the company :

- failure to appoint a statutory auditor or to certify information in terms of sustainability (€30,000 fine for the director + 2 years' imprisonment and €150,000 fine for the company)

- in the event of obstruction of the auditors' verification and control of information in terms of durability or refusal to communicate documents useful to their mission (€75,000 fine for the director + 5 years' imprisonment and €375,000 fine for the company)

It should be noted that the implementation by 2026 of the CSDDD, reinforcing the obligations linked to the duty of vigilance (due diligence) of companies in terms of preserving the environment and respecting human rights, may broaden the possibilities of sanctions to which companies will be subject. In particular, financial penalties could, like those linked to the RGPD, correspond to a percentage of the sales of the company concerned.

How to prepare your company for CSRD?

If your company was already subject to the NFRD, the big change ahead for you will be the obligation to report on a CSR strategy to reduce impacts.

If this is the case, you will have to start collecting ESG data at the beginning of 2024, so that you can postpone the deadline until January 1, 2025. To get a head start, you can, among other things :

- Ask yourself about the place of your company and the role it can play in the energy and ecological transition,

- Identify risks and impacts on ESG criteria,

- Collect initial ESG data (the carbon footprint is one example),

- Prepare a CSR strategy to reduce your impact.

Anticipating the ESG data collection process

The first phase in preparing your CSRD reports will involve collecting the hundreds or even thousands of items of data that will be used to complete your reports, refine your analyses and build your action plans.

Companies that have already drawn up a carbon plan are well aware of the difficulties involved. The advantage for their teams is that they have already done most of the work. The environmental aspect, and in particular the ESRS E1 standard dedicated to the climate, is the one that will require the most commitment and involvement from the finance and CSR departments.

The difficulty lies not only in the quantity of data that needs to be collected, but also in its diversity. ESG data is distributed throughout your value chain. Internally, all your company's sites and departments have access to the information essential for compiling your reports.

The same applies to your suppliers, service providers, etc., who will also contribute to measuring your carbon footprint on scope 3 upstream and scope 3 downstream.

We strongly advise you to use a tool that can support you in the process of collecting and processing ESG data, to simplify and clarify the process.

Prepare your dual materiality analyses

As we said earlier, materiality analysis will form the basis of your reporting.

For each of the reports requested, you'll need to carry out this analysis, which will enable you to measure your impact on the subject in question, as well as the impact it may have on your business, whether physical or financial.

If a topic is considered "non-material" to your business, you won't have to report on it. Nevertheless, reporting on climate change will be almost inevitable, as any activity has an impact on the climate, or can be impacted by it in various ways.

If you decide to bypass this reporting, you'll need to be able to justify it with a full explanation of your analysis method.

Building an action plan

The CSRD requires you to implement action plans to reduce your impact (negative, of course) on the various indicators.

In the context of climate change, the latter is particularly well-defined. It must follow a scientific method, and be in line with the 1.5 degrees of global warming target set by the Paris Agreement, and with the goal of carbon neutrality at European level by 2050.

Not only is this action plan highly restrictive, it will also be scrutinized by financial market players in a context where the European Union is strongly encouraging investors to redirect their investments towards companies that are virtuous in terms of environmental transition.

An action plan that is too unambitious or lacking in credibility will send the wrong signal to the market. A risk that's best avoided at the risk of being shunned by investors, buyers, consumers or any other stakeholder in the company.

Mobilizing resources for long-term action

The CSRD is an annual exercise, requiring data collection, impact analysis and modeling of an action plan with follow-up year after year.

Randomly compiling a carbon footprint on an Excel file will no longer suffice. You need a reliable tool that can support your company over the long term, enabling you to collect and process data, carry out in-depth impact analyses, implement an action plan and anticipate its effects and costs.

The solution developed by Traace is able to provide you with all these elements to publish your CSRD reports, via a data collection module enabling you to centralize and process all the data collected throughout your value chain. A modeling tool will enable you to define and manage your action plan. You'll be able to visualize the performance of your actions on your GHG emission levels, as well as the short, medium and long-term financial impact of each of the levers you can activate.